Credit Card Payment Processing

Credit card payments, online payments, and mobile-optimized options will be increasingly important to merchants in the coming years. Are you offering customers the payment methods they prefer?

Read on for information about how we got here, how a credit card is processed, and industry/legal requirements your business must follow while taking credit card payments.

In This Guide

- History of credit card processing

- How credit card processing works

- Credit card compliance

- Credit card processing fees

- Credit card processing security

Ready to streamline payments, digital document delivery, and eSignatures—all from one platform? The Cable Team can help. Send documents, collect eSignatures, and process payments securely via email and SMS with Flow Technology.

A Quick History of Credit Card Processing

The concept of credit cards began in the 1920s with “courtesy cards” used by large U.S. businesses (like hotel chains and oil companies) to allow customers to charge purchases at their stores.

In 1950, Diners Club introduced the first credit card that could be used at multiple locations. Frank McNamara, who forgot his wallet at a restaurant, came up with the idea that launched this multi-store card. By 1951, 20,000 people held Diners Club cards.

American Express introduced a charge card in 1958. Later that year, Bank of America launched the Bank America —the first revolving credit card that allowed consumers to carry a balance.

In 1976, Bank America became Visa, and Master Charge became MasterCard. The credit card industry grew rapidly, and consumer protections followed, like the Truth in Lending Act (1968) and the Fair Credit Reporting Act (1970).

The 1980s brought cash-back rewards with Discover. In 2009, the CARD Act limited penalties and fees on credit cards.

Today, Visa and MasterCard operate some of the largest card networks in the world.`

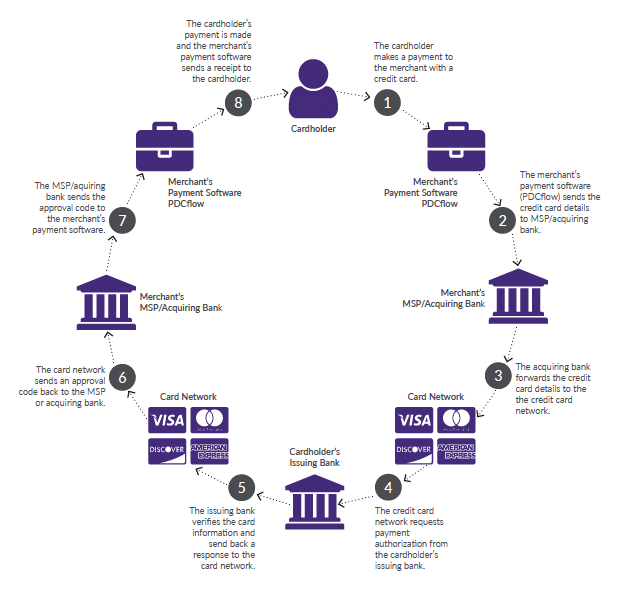

How Credit Card Processing Works

Each card transaction involves several key players:

- Cardholder – The customer using a credit card

- Merchant – The business accepting the payment

- Acquiring Bank – The merchant’s bank that processes credit card transactions

- Issuing Bank – The customer’s bank that issued the credit card

- Credit Card Networks – Visa, Mastercard, Discover, American Express

- ISOs and MSPs – Third-party processors and merchant service providers

Transaction Flow:

- Authorization:

The cardholder initiates a payment, and the merchant transmits the data via a payment gateway to the processor/acquiring bank. It goes through the card network to the issuing bank. - Approval:

The issuing bank verifies the transaction, checks for fraud, and sends approval/denial back through the network to the merchant. - Batching:

At the end of the business day, the merchant submits all approved authorizations as a batch. - Settlement:

The issuing bank sends funds (minus fees) through the network to the acquiring bank, which deposits them into the merchant’s account.

Payment Terms to Know

- Card Not Present (CNP): Online or phone transactions without a physical card

- Chargeback: Disputed transaction reversed by the issuing bank

- Interchange Fee: Charged by the card network and paid by the merchant

- Merchant Discount Rate: Total percentage taken from each transaction

- Payment Gateway: Software that transmits transaction info securely

Credit Card Compliance

Merchants must follow security rules known as PCI DSS (Payment Card Industry Data Security Standards), developed by the PCI Security Standards Council.

Your compliance obligations depend on:

- Transaction volume

- Whether you store cardholder data

- Tools and software you use

Choosing a PCI Level 1 Compliant Provider like The Cable Team simplifies compliance and reduces risk.

Additional Legal Requirements

If you accept debit cards and ACH payments, you must comply with:

- The Electronic Funds Transfer Act (EFTA)

- Regulation E, which requires written and signed authorization for each debit

These apply even for one-time transactions.

Understanding Credit Card Processing Fees

Fees vary depending on your provider, card network, transaction method, and your contract terms.

Common Fees Include:

- Interchange & Network Fees

- Monthly Statement Fees

- PCI Compliance or Non-Compliance Fees

- Address Verification (AVS) Fees

- Chargeback & Retrieval Fees

- NSF (Insufficient Funds) Fees

- Early Termination Fees

Pricing Models:

- Interchange-Plus: You pay actual interchange cost + a fixed markup. Transparent and itemized.

- Tiered Pricing: Bundles transactions into Qualified, Mid-Qualified, and Non-Qualified groups. Less transparent.

- Zero-Cost Processing: You pass transaction fees to the customer (legal review recommended).

Security in Credit Card Processing

Card-not-present (CNP) transactions—especially online—are more prone to fraud. Secure technology from The Cable Team minimizes this risk.

Key Security Features:

- Tokenization: Replaces card data with secure tokens so you don’t store sensitive info.

- Encryption: Scrambles transaction data in transit to prevent theft.

- Secure Vault: Card data is stored off-site, reducing your PCI scope.

Final Thoughts

The Cable Team offers merchants a secure and compliant way to accept credit cards and ACH payments, while also delivering eSignature and digital document solutions.

With The Cable Team, you can:

- Build seamless payment workflows

- Improve customer experience

- Simplify compliance

- Protect your business from fraud